At some instances in our lives, we usually need some financial help from external sources. In addition, we may even need a loan that we will be able to pay in small bits for an extended period.

Suppose you need to sort out some emergency needs, which will require lots of cash in the picture. In this case, a payday loan will not help you. Instead, you will enter into unnecessary pressure to repay the loan after two weeks.

And that’s where installment loans come into play. With installment loans, you will pay the loan in a more extended period.

In this guide, I will show you how you can apply for installment loans. And you will have a humble time the moment you head to your lender.

But first, what are installment loans?

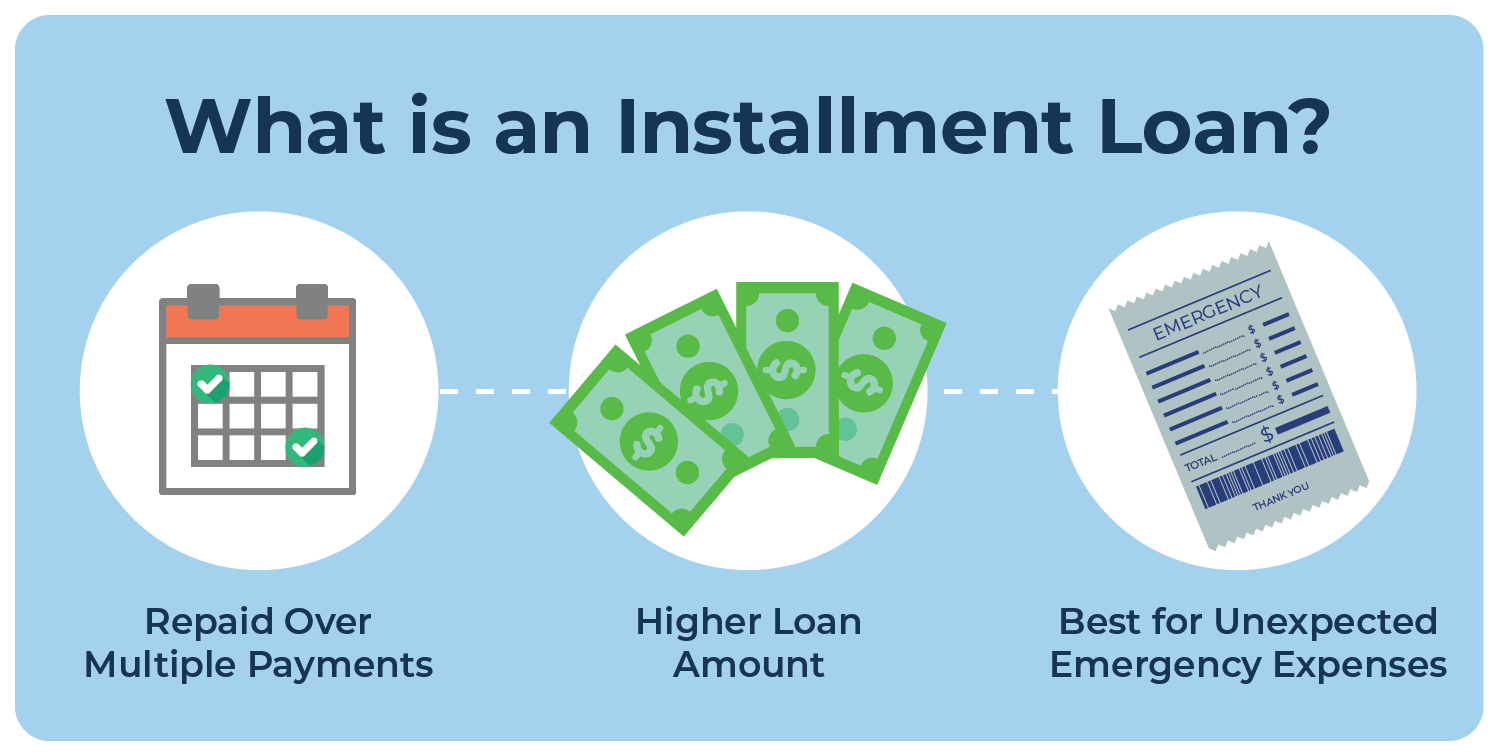

Like I have said, an installment loan is a kind of loan that you apply for cash in a lump sum and then repay in small bits for an extended time. In most instances, you will negotiate with your lender on what amount your installments should have.

In each installment, there is usually a percentage of the principal amount and another one for interest. So, for instance, if your total repayment is $1000(inclusive of the rates), the lender may divide that amount into equal installments.

Types of installment loans

As long as you take a loan in a lump sum and pay it back in small bits, then that’s an installment loan.

-

Personal loan

This is a loan that you sign against your name, and you can use it for whatever reason you want. In most cases, personal loans are unsecured. Therefore, you will not provide any collateral to get a loan. However, you will have to sign against your paycheck for the lender to deduct the money automatically each month.

-

Auto loans

These are loans that you take to buy a car. You cannot use the money for anything else apart from the vehicle. Once the lender approves the auto loan, you will start paying in small installments till you complete the payment. In this loan, the car stands as security, and if you default, the lender takes the car to regain its funds.

-

Mortgages

You can only take a mortgage loan if you want to buy a house. But, like an auto loan, the home here stands as security if you fail to repay the loan. Once you take a mortgage loan, you will pay in small installments for more than 15 years.

How to apply for an installment loan

Are you wondering how you can start to apply for an installment loan? Well, I got your back. But first, here is what to consider before you go ahead with the application.

Do you need an installment loan?

This question should be the first that comes to your mind if you are considering taking an installment loan. I will advise you to take the loan that you need at the moment. There is no logical reason to take an installment to spend on luxurious things.

List down the reasons that you would like to apply for an installment personal loan. Is it worth it? Let’s not talk about auto loans or mortgages since you can’t misuse the funds. But as for personal installment loans, you should be more careful.

Compare interest rates

After you decide what you should do with your installment loan, you should first compare the interests. Whether you are applying for auto, mortgage ott personal installment loans, you should first compare interest rates from different lenders.

Do not rush into deciding to take an installment loan. It’s possible to get installment loans with lower interest rates. So go for them

Does the lender have a valid operation license?

This is something else that you should look into if you want to be safe with your money. For instance, if you are taking a secured installment loan, you should 3nsure that you see and validate the lender’s license. That way, you won’t put your property documents at risk.

How long will you repay the loan?

It’s essential to know the period at which you will spend paying off your installment loan. This criterion will help you in making a proper budget for your finances.

In addition, you will know how much you will be able to save each month. In addition, if you want to repay your loans faster, you can adjust the repayment period with your lender.

However, doing so will lead to paying more money in installments and paying for a shorter period. Therefore, you should ensure there are several income sources before you make that decision.

All extra costs

Some lenders will charge you establishment fees before you can take a loan from them. Therefore, it’s essential to know the associated costs and how much you will take home.

Some other costs include early repayment fees and late repayment fees. Lenders may charge you early repayment fees. In contrast, other lenders will charge you late repayment fees if you default from paying your installment loans.

Now, with all that information in mind, you will have the idea to choose the best lender.

So, where do you get installment loans?

-

Traditional banks

The first place where you can get installment loans is in traditional banks. After that, you will have to go to your bank and apply for an installment loan personally. The processing period depends on whether you need a personal, auto, or mortgage loan.

-

Online lenders

With the growth of Fintech, online lending is growing day in day out. You can log in to your favorite lending site after considering the factors mentioned earlier.

Then, apply for an installment loan with just a few clicks. With online lenders, you can access the loans from the comfort of your home

-

Credit Unions

You can still get an installment loan from credit unions. However, the installments with these lenders are usually small. But they are good when you have a bad credit score.

Endnote

As much as it’s easy to get an installment loan, you should be careful only to take funds that you can manage. Remember, taking what you can’t manage can lead you to serious money problems.

CHECK: